Do you work in the Canadian construction industry? If so, there is a good chance that you’ve heard the term surety at some point. Unfortunately, you probably did not understand the term at the time. You were likely confused. Well, it would be a good idea to seek education. After all, you’re working in the construction industry and you’re likely going to rely on surety from time to time. Surety bonds make it possible for one party to hold another one liable. This makes them liable for many things such as a debt, failure, or detail.

If you assume the role of a contractor, you’re likely going to be required to obtain a surety bond. To acquire a bond, you will need to work with an insurance company. That company will warranty or guarantee your work. Basically, the insurance or surety company will become your co-signer and they’ll help protect your customer. In Canada, a surety is the party that agrees to assume responsibility for another individual.

What It Means For A Surety

Ultimately, the surety company is going to be responsible for your company. They are putting up collateral for your company and you will be required to pay a monthly premium. The surety is there to say that you’re going to get the job done on time and as specified in the contract. If you fail to live up to your end of the bargain, a claim can be filed against your surety bond. Then, the surety company will need to step in and solve the problem.

They will investigate the situation and solve the issue using the method they see fit. The surety protects the client in many situations. If the project does not get completed or isn’t completed on time, the surety bond will prove to be very beneficial for the client. Your company will pay a premium to obtain the surety’s backing.

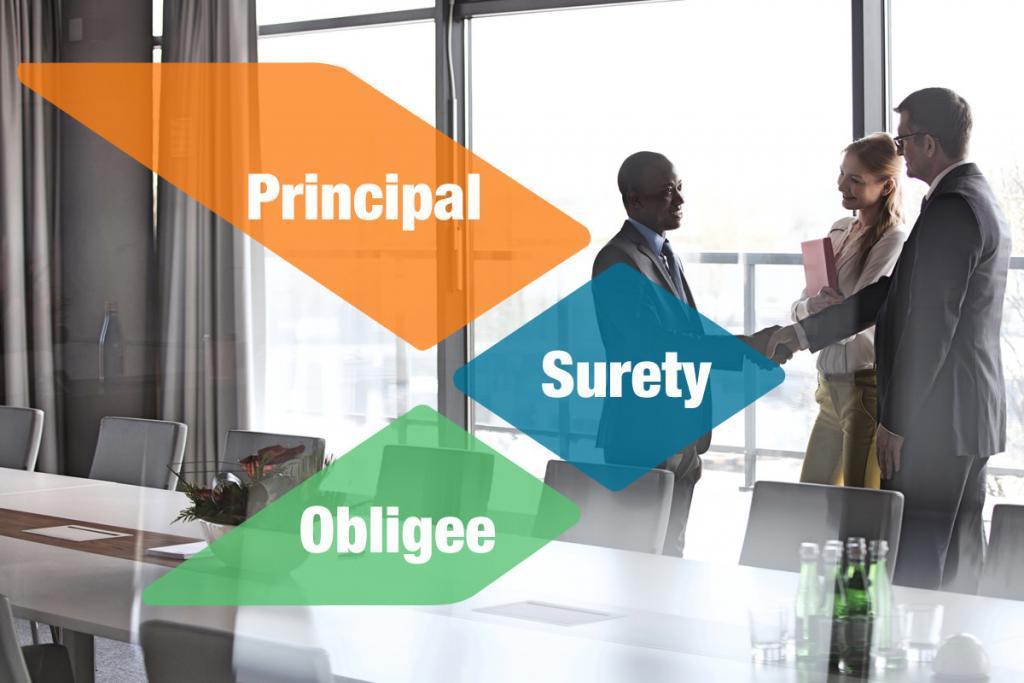

Three Parties Involved

It is important to understand that a surety bond will include three parties. Whether you’re dealing with construction bonds, license bonds, or another type of bond, there will always be three parties involved. The first is the principal. You’re the principal and you’re required to obtain the bond. Usually 3 types of required during construction project. The bonds required are bid bond, performance bond, and or labour and material bonds in addition to a performance bond.. In other words, your company is going to be insured by the surety company. You will be required to obtain the bond by the obligee. This is your client.

It is the party that is protected by the bond. Finally, there is the surety. This is the company that sold the bond and they’re responsible for ensuring that the company gets the job done right and on time. The bond protects the client and vouches for the company. Therefore, it can be very beneficial for both parties.

Where To Get Bonded In Canada?

Regardless of your social class, you can get bonded in Canada. If you are contemplating starting a business, offering a service, or increasing your existing business’ customer base, the best way to start is with a surety bond. Many insurance companies underwrite surety bonds. Depending on the type of surety bond you are looking for, two or three parties are involved in the process. Most surety bonds require three parties – the principal, obligee, and surety. Others only require two parties – the surety and principal.

The principal is responsible for obtaining the surety bond. But, the surety bond generally protects the obligee more than the principal. It does this by making sure the principal is a suitable candidate. The surety company is also responsible for protecting the obligee. By making sure the principal is trustworthy, legal, licensed, and capable of fulfilling the terms of the bond, the surety is doing its part to protect consumers from becoming victims of fraud.

The best way to find insurance companies that underwrite surety bonds is to conduct a brief Google search. You can also utilize your local phone book as well.